By Cesar Perez-Carballada

The media and advertising landscape are changing fast. Although TV is still prevalent, digital is growing fast and most of the other media are decreasing their preponderance, but will digital continue growing indefinitely? What will happen to the TV in the long term? What trends will affect overall advertising spending?

We will explore these and other questions in this series of two posts which will try to approximate the next decade by looking at the past 80 years of advertising.

Part 1: past and current advertising evolution

Part 2: the future of advertising

PAST AND CURRENT ADVERTISING EVOLUTION

We all know that consumers’ habits are evolving: consumers already spend more time consuming digital than traditional media in every country in the world except in five: the US -where linear TV enjoys an enduring popularity- and a clutch of Western European markets (Belgium, France, the Netherlands and Germany) where the relative lack of enthusiasm for social networks decreases the impact of digital (1).

That data comes from a global survey which is carried out annually in 34 countries and although the sample size is large (a total of 350,000 respondents), someone can argue that a self-reported estimate is not an accurate source for media consumption that’s why it makes sense to look at other sources such as Nielsen, which don’t ask but directly track people’s behavior. According to Nielsen, adults spend 686 minutes every day consuming media in the US: that’s more than 11 hours per day (figure that is remarkably close to the self-reported numbers in the prior survey). As we can see in the next chart, TV still represents almost half of that consumption, while smartphones, tablets and PC (all together) get slightly more than one-third of it. Yet, the trend is clear: although TV preserves its leadership, it is losing its relative weight to digital, which is growing faster. Even more, young adults already consume more digital than TV (2).

Almost all the media consumption growth in 2016 was driven by digital and 88% of all growth was due to smartphones, which represent now 22% of total time spent with media. According to Jonathan Barnard from Zenith, that is happening because smartphones turned “what used to be a non-media activity (e.g. talking to friends and family) to media activity (e.g. social media).” (3)

Analysts say that the total media consumption is still growing (+1.8% expected growth in 2017 vs 2016) but it is reaching a limit: there are only so many hours in the day. Therefore, all future major growth in one medium will likely come at the expense of another (3).

In terms of advertising trends, overall ad spending is expanding at a rate of 4.4% each year in the US, according to Zenith Media (4). TV is still dominant but digital is growing dramatically, mostly at the expense of print (see next chart).

After looking at these numbers, some unanswered questions remain, for instance, will digital continue growing indefinitely? What will happen to the TV in the long term?

In order to answer those questions, we can look at the past evolution of media and identify the drivers behind it. To do so, we should not only consider the short term but the long run: what do the past 80 years tell us about the next decade?

THE HISTORY OF MEDIA AND ADVERTISING

When we look at the past 80 years of advertising spending we find certain patterns (see next chart)(5).

After many years during which print was the only relevant medium, the first radio ad aired in the US in 1922 (6) and its unique offering to advertisers (audio) made its share of advertising spend to grow from zero to 20% over the next 20 years. After World War II, the radio had a partial setback when the FCC decided to move up the FM spectrum making every FM radio in the country obsolete and killing off the audience that FM had developed (7), paving the way for the initial TV stations. The advent of television advertising provided advertisers with the ability to deliver more engaging messages to consumers with both video and audio which drove TV's share of advertising spend from zero to 32% in 35 years. TV advertisement plateaued at 34-37% during the next 30 years while outdoor enjoyed a small revival and print continued declining. Then internet and smartphones emerged: digital platforms provided advertisers with the ability to deliver messages to targeted groups of consumers in a way that traditional media could not, which has driven its share of advertising spend from zero to 32% in 20 years.

The dominant advertising growth currently enjoyed by digital platforms mirrors the growth phases of previous "disruptive" media -radio and television- with only one difference: its speed. While radio grew at ~8% CAGR in 1935-1949 and TV expanded at ~14% CAGR in 1949-1984, digital has grown at 33% CAGR between 1995 and 2016. There is another difference. Like radio’s and TV’s emergence, digital’s took a toll in print’s share but digital has done so at a whopping speed bringing print down not only in relative terms (it went from 46% of the total in 2000 to only 18% in 2016) but, more worryingly, also in absolute terms (print lost half its revenues during the past decade)(5).

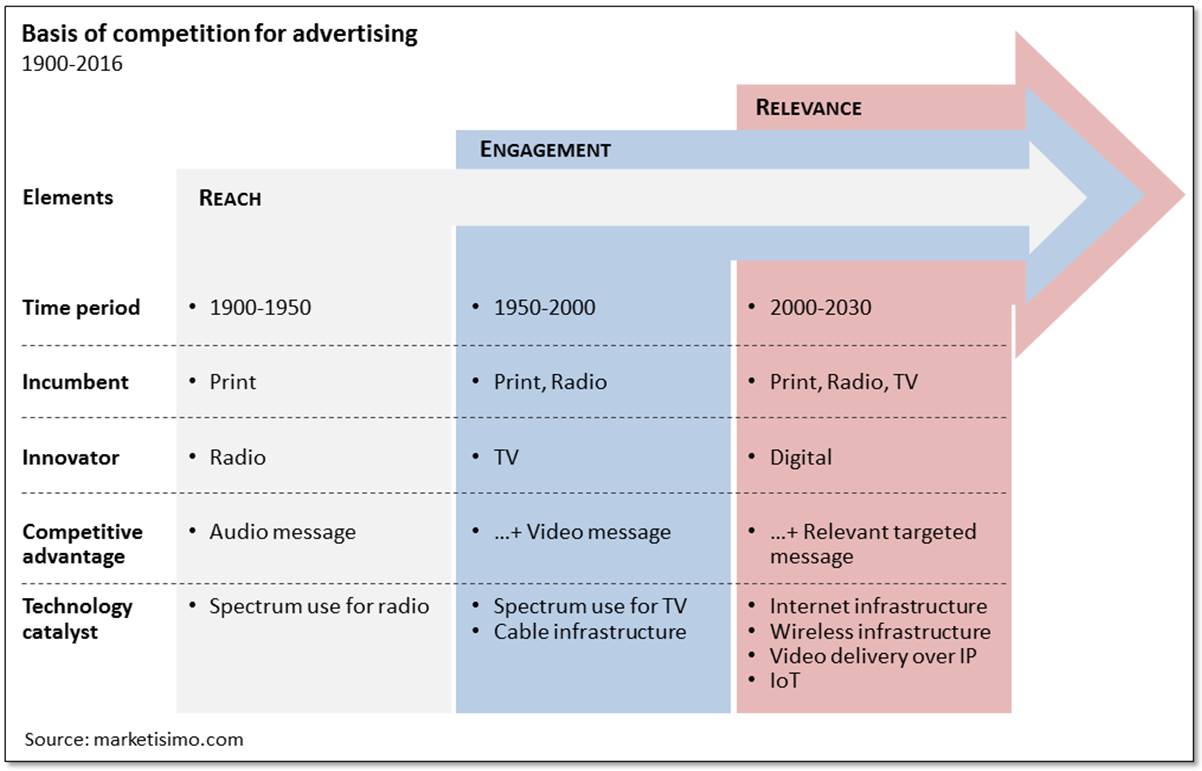

THE BASIS FOR COMPETITION

Eighty years of advertising history shows us that the basis of competition for advertising products has changed over time. Suppliers (i.e. media owners) have evolved from competing on the basis of just ‘reach’ (1920-1950) when platforms simply offering access to the greatest number of consumers won share; to ‘engagement’ (1950-2000), when access to consumers had become ubiquitous and communicating with an engaging message including both audio and video became the primary driver of share gains. Since 2000, we have been in a period when ‘relevance’ is a new basis of competition, i.e. targeting consumers with a tailored message is a key differentiator between platforms.

Thus, advertisers who originally looked for ‘reach’, then also added ‘engagement’ to their requests -which explains the huge success of TV- and finally, they also started asking for ‘relevance’ -which explains the rapid growth of digital-. Of course, cost was an underlying factor along the way but media was typically priced based on the other three variables (e.g. CPM adjusted by engagement and relevance) thus those said elements were the independent variables guiding the media selection.

Nowadays, all media compete along the three variables: ‘reach’, ‘engagement’ and ‘relevance’.

Digital advertising – including search, social, online video and display – is rapidly improving its performance for advertisers. With relevance its natural strength from inception, it has steadily added reach so that today it has a formidable combination of both (the “sweet spot”). Moreover, digital advertising's reach and relevance continue to improve, so if left unchecked, the medium in aggregate could at some point in the future surpass the overall performance of TV. We know that digital's share of ad spend is already ahead of TV's in some global markets such as the UK and China but here we highlight the possibility that it could become a credible substitute for TV if TV does not itself move to the right in the matrix (see prior chart) by improving the relevance or targeting of its messages.

In that context, the advances being made in the US TV industry to introduce much closer targeting of video advertising (e.g. Open AP) are important for the future development of TV advertising because, if successful, targeted video advertising could shift TV advertising to the right in the reach/relevance matrix which would position it to win market share, but if unsuccessful, could leave TV advertising vulnerable to continue losing share to digital.

Having reviewed the past and current status of media and advertising, what can we say about their future? That will be the focus of the second and last post of this series.

Tweet

___________________________________________________________

- Share here you opinion of this article

- Send this article by email

___________________________________________________________

Sources:

(1) Global Web Index, Insights Report Summary, Q1 2017

(2) The Nielsen comparable metrics report, Nielsen, Q4 2016

(3) People consumed more media than ever last year - but growth is slowing, recode, Rani Molla, May 30th, 2017

(4) Adspend Forecast, Zenith, retrieved July 5th, 2017

(5) The Future of advertising, Credit Suisse, April 25th, 2017; Zenith media website, retrieved July 2017

(6) First Radio Commercial Hit Airwaves 90 Years Ago, John McDonough, NPR, August 29, 2012

(7) History: 1940s, AdvertisingAge, September 15, 2003

(8) The Nielsen comparable metrics report, Nielsen, Q4 2016; eMarketer US Mobile Time Spent and Activities StatPack 2017, May 2017; eMarketer report April 2016 (via Heidi Cohen); Adspend Forecast, Zenith, retrieved July 5th, 2017

(9) How Ad Tech Just Might Save TV, AdvertisingAge, Jeanine Poggi, February 21, 2017

(10) Internet Trends 2017, Mary Meeker, Kleiner Perkins, May 31, 2017

(11) Digital is reshaping the world of advertising, Shannon Bond, Financial Times April 28, 2015

___________________________________________________________

Author: César Pérez Carballada

Article published inhttp://www.marketisimo.com/

No comments:

Post a Comment