By Cesar Perez-Carballada

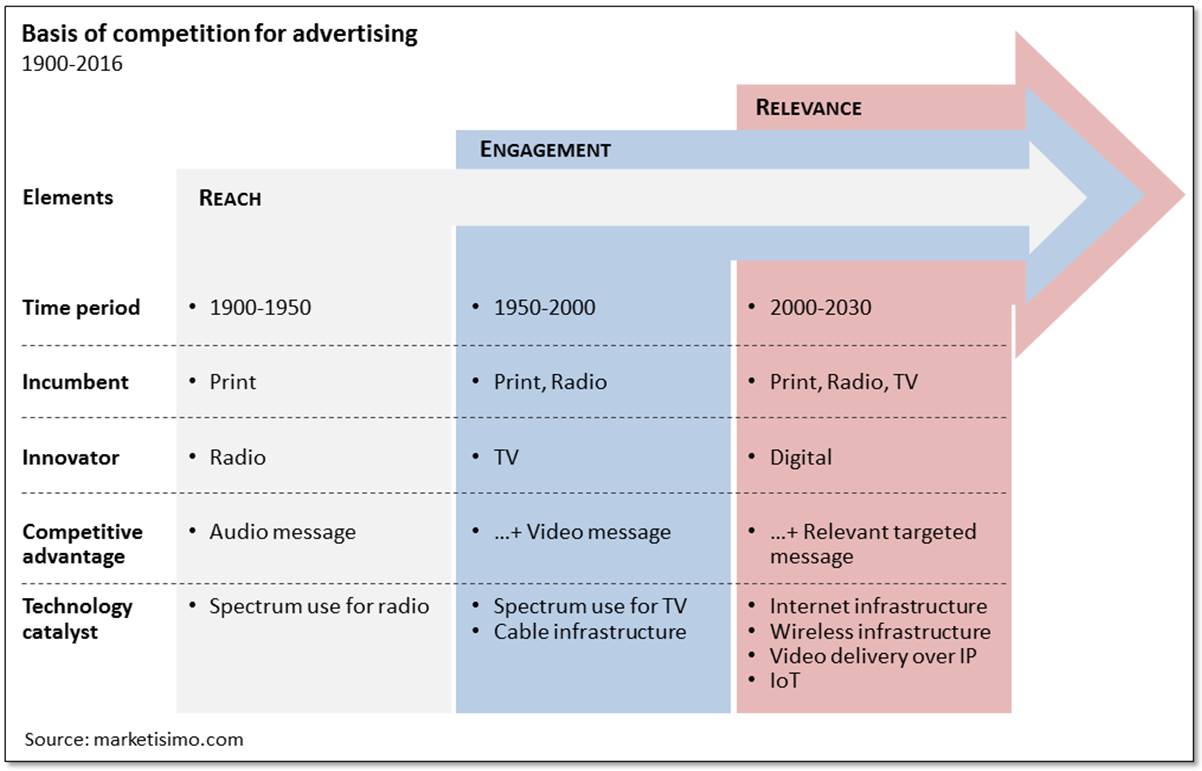

This is the second post of the series. In the prior one, we analyzed the advertising evolution during the past 80 years and how the basis for competition has changed (from “reach” to “relevance”). Now we will assess what will happen to the media and advertising mix in the future.

CURRENT AND FUTURE TRENDS

In assessing the future outlook of the advertising industry, there are 3 relevant trends that we might consider as follows:

(1) Imbalance between media consumption and advertising spending

Advertising spending should be aligned (given that all other variables are the same) with the media consumption. For instance, if consumers devote 30% of their time to watch TV, advertisers should spend 30% of their budget on TV. Of course, the media’s engagement and relevancy also affect advertisers’ preference but if there is a large discrepancy between media consumption and ad spending, time will tend to eliminate it by adjusting ad spend. Current imbalance is as follows (*)(8):

As we can see, in spite of its rapid growth, digital is still underrepresented in terms of ad spend while print, in spite of its fast decline is still overweighed. These imbalances might get even bigger over time because consumers are increasing their digital consumption at the expense of other media. Therefore, these imbalances suggest that digital’s ad spend will continue growing rapidly at the expense of print and other minor media while TV is expected to keep the same level.

(2) IoT and Machine Learning

These two technological developments have been maturing during the past few years and are reaching momentum. They will impact advertising by increasing the relevance of ads to consumers: (i) the Internet of Things will multiply the number of devices giving advertisers direct access to consumers, and (ii) advancements in machine learning will allow advertisers to use the data gathered from IoT and other connected devices to better target advertising messages.

Thus, wearable health trackers, connected cars, connected home control devices and connected appliances will all provide advertisers with a step-change in two ways. First, their usage will provide new platforms through which consumers can be reached. For example, a fast food advertiser will be able to reach a potential customer in their connected car with an offer as she approaches a drive-thru restaurant. Perhaps more importantly, connected devices will also provide valuable data on the purchase habits, movements and location of consumers which can inform all marketing, not just the messages delivered on the connected devices themselves. These developments further underline the importance of direct access to consumers via platforms on which they spend time, as ownership of usage data will provide opportunities to deliver more efficiently-targeted advertising. This will further benefit media that are naturally “connected” to consumers such as digital platforms. It may benefit TV networks and content developers if they integrate vertically to gain direct access to consumers (e.g. NBCU+ with Comcast, Time Warner with AT&T) and if they develop a more targeted approach to guide their advertisement offering (e.g. Open AP).

(3) The emergence of targeted linear TV advertising

Over the past years, TV networks in the US have been building their ability to improve the relevance of their advertising products. One example is 21st Century Fox, Turner and Viacom which launched Open AP in April 2017. Open AP is an advertising platform which allows advertisers to use their own data along with data from third parties to define narrow target audiences for ad purchase across the networks of all three partners: instead of targeting, for instance, “men aged 18-34”, advertisers can now target “"truck owners whose lease is about to expire".

More effective targeting has also the potential to improve the user experience in linear TV: the number of ads to reach the same net GRPs (TRPs) can be substantially reduced, thus ad loads can be reduced from 18-20 minutes per hour to 2-5 minutes per hour of better targeted ads or even to 60 seconds per hour of interactive ads (9), reducing the gap in user experience relative to SVOD platforms. This approach will add ‘relevance’ to the already considerable ‘reach’ of TV advertising (moving TV towards the sweet spot at the top-right in the reach-relevance matrix). Better targeting suggests that TV should be able to capture a greater share of advertising spending over time. If networks stand still and do not improve their offering to advertising customers with greater targeting to complement their reach, they risk allowing digital advertising to eventually become a substitute product.

THE FUTURE OF MARKETING

Based on the above trends, analysts estimate (5) that overall marketing spending, both ATL (Above-The-Line) and BTL (Below-The-Line) will grow at 3.5% per year between 2017 and 2030 but ATL will grow at 6.4% CAGR, which means that BTL will barely grow and will reduce its share: media consumption’s trend, proliferation of IoT devices and the development of machine learning will enable digital and targeted TV to take share not only from print and radio but also from other below-the-line spending.

In general, we should not expect big changes to ‘brand building’ expenditure (5), with investment shifting into digital, TV, PR and sponsorship and we can expect the growth in the latter two (often forgotten) items will outpace the growth in overall marketing spend.

There are much bigger chances of changes, however, to come in ‘call to action’ spending. 44% of US marketing investment in 2016 was in this category, including price promotions, direct mail and telephone marketing. The proportion spent on price promotions may remain unchanged in 2030 (at ~20% of total marketing spending) but spending on direct mail and telephone marketing might migrate to digital platforms and targeted TV because advertisers will be able to use machine learning on data generated from connected devices to analyze consumers' habits, preferences, location and purchase patterns, to learn which advertising messages might work best and to deliver them on digital and targeted TV platforms wherever consumers may be (something that neither direct mail nor telemarketing will be able to do). For this reason, we can consider those media as substitutes for direct mail and telephone marketing, and expect virtually all of today's investment in these two items (~$106bn) to migrate to digital and targeted TV by 2030 in the US (5) if the current trend continues. We could argue that ‘call to action’ spending on print, radio, outdoor and cinema will be virtually entirely squeezed out.

In other words, advertisers may deploy their ‘call to action’ spending to either (i) highlight where or how to purchase a product via a connected device – which could be a connected car, a connected screen, a wearable, a connected home appliance or connected clothing; or (ii) offer a short term price discount.

THE FUTURE OF ADVERTISING

The consequence of the above dynamics is that overall ad spending (ATL) will grow faster than the recent historical rate (6.4% 2017-2030 vs 4.8% 1980-2016) but in line with the past 80 years trend (see next chart)(5)

However, ad spending in each medium will evolve in different ways, some of them will capture share while other will lose it, as follows (5):

As we can see in the prior chart:

(1) Digital will be the main winner of the next decade , adding ‘reach’ to its traditional strong ‘relevance’ and, in some cases, improving ‘engagement’ , growing to capture ~55% of the ATL market. In this way, digital will achieve the fastest growth for any medium in the last 100 years (11-13% CAGR 2017-2030) although at a lower rate than in the recent years (~16% CAGR 2000-2016). Actually, digital will very likely surpass TV in the US for the first time in 2017.

(2) Given its large ‘reach’ and ‘engagement’, TV has better chances to resist the advance of digital and it can retain its current share (36-37% of total ATL) and increase its absolute size (5-7% CAGR) given its future ability to gain share of ‘call to action’ spending as long as it improves its ‘relevance’ with better targeting tools.

(3) Outdoor will slightly decline its share of total ATL spending but will grow in absolute terms by 2-3% CAGR, mimicking its historically performance.

(4) Print and radio will continue declining due to their weaknesses in terms of all the key variables (reach, level of engagement and relevance) although print will fall faster than radio (-11% vs. -7% CAGR respectively). Some niche medium can survive but, all together, these media will become marginal in the advertising industry with ~3% of the total ATL spending.

The conclusion that digital will continue growing is hardly surprising and many experts agree, however the conclusion for TV is divergent from other forecasts (according to ZenithOptimedia and Magna Global, TV advertising will decrease around -0.6% per year 2017-2019). Contrary to those forecasts, we can anticipate that TV advertising's growth rate can actually improve provided that it increases its relevance via innovative targeting tools.

IMPLICATIONS FOR ALL STAKEHOLDERS

Digital platforms are intrinsically better positioned to deliver relevant advertising and, as they grow in size, are on a near-inexorable path to take share from all parts of marketing budgets. This situation will benefit digital platforms, mainly Google and Facebook which captured ~70% of total digital spending in 2016 and 85% of its growth (10).

TV networks are improving their ability to deliver targeted advertising on linear inventory which could put them in a strong position to compete with digital platforms, sustain share of overall advertising spend and to grow advertising revenues faster than we have seen in recent years. This condition would benefit media companies with high exposure to TV advertising such as Viacom, CBS and Twenty-First Century Fox in the US, while vertically integrated networks/distributors such as Comcast and AT&T-Time Warner would be in a stronger position to capitalize on the targeted TV advertising opportunity.

Agencies should not see a material impact since they will still have a pivotal role in media buying and planning as well as in creative content creation. In spite of the media changes, clients will still need agencies for guidance in a cross platform media world. However, digital ad fraud (6% of online video impressions, according to comScore) and the digital media supply chain leakage (up to 60% of the digital spend, according to WARC)(5) may require a clean-up of the supply chain and the imposition of more transparent contracts, which is likely to be painful for the agencies, with Publicis, Omnicom and WPP being the most sizeable in digital media buying.

Finally, advertisers will need to develop the capabilities required to adapt to the new advertising world. Digital becoming the ‘de-facto’ medium and more targeted TV will require better skills in data analytics. The main challenge for advertisers will be to “digest all the different pieces of data they’re getting: loyalty card and customer relationship information, a blitzkrieg of data from social channels, clicks, Facebook,” says Drew Panayiotou, former Best Buy CMO (11). Thus, advertisers will need to extract insights from disperse data sources for which they will have to develop new skills.

*****

If the past can inform the future, we know that advertising will continue growing and that digital will be the winner concentrating such a dominant share of the advertising spending which is unheard of since that of print in the 1960s. Linear TV will depend on itself to keep its share and the other media will have to adjust to the new reality.

Independently of any forecast, the only certainty is that we will face a cross-platform world which will require to develop capabilities that are much more complex than the ones needed in the past. Are you ready for this new reality?

___________________________________________________________

- Share here you opinion of this article

- Send this article by email

___________________________________________________________

Sources:

(1) Global Web Index, Insights Report Summary, Q1 2017

(2) The Nielsen comparable metrics report, Nielsen, Q4 2016

(3) People consumed more media than ever last year - but growth is slowing, recode, Rani Molla, May 30th, 2017

(4) Adspend Forecast, Zenith, retrieved July 5th, 2017

(5) The Future of advertising, Credit Suisse, April 25th, 2017; Zenith media website, retrieved July 2017

(6) First Radio Commercial Hit Airwaves 90 Years Ago, John McDonough, NPR, August 29, 2012

(7) History: 1940s, AdvertisingAge, September 15, 2003

(8) The Nielsen comparable metrics report, Nielsen, Q4 2016; eMarketer US Mobile Time Spent and Activities StatPack 2017, May 2017; eMarketer report April 2016 (via Heidi Cohen); Adspend Forecast, Zenith, retrieved July 5th, 2017

(9) How Ad Tech Just Might Save TV, AdvertisingAge, Jeanine Poggi, February 21, 2017

(10) Internet Trends 2017, Mary Meeker, Kleiner Perkins, May 31, 2017

(11) Digital is reshaping the world of advertising, Shannon Bond, Financial Times April 28, 2015

___________________________________________________________

Author: César Pérez Carballada

Article published inhttp://www.marketisimo.com/ Continuar leyendo el resto del artículo...